Chapter 6 Advanced Features

6.1 Introduction

As seen in previous chapters, INLA is a methodology to fit Bayesian hierarchical

models by computing approximations of the posterior marginal distributions of

the model parameters. In order to build more complex models and compute the

posterior marginal distribution of some quantities of interest, the INLA

package has a number of advanced features that are worth knowing. Some of

these features are also described in detail in Krainski et al. (2018).

In this chapter we will describe some of these features. In particular, Section

6.2 shows how to define a predictor matrix that multiplies

all terms in the linear predictor, so that the actual linear predictor of the

model is a linear combination of the effects in the model formula. Next,

Section 6.3 presents how to define linear combinations of the

latent effects to compute their posterior distribution. Section

6.4 introduces the use of models with several likelihoods.

Models with several likelihoods that share some terms are in Section

6.5, where the copy and replicate features are described

in detail. These features are very useful when working with, for example, joint

models (see Chapter 10).

6.2 Predictor Matrix

The formula passed to the inla() function defines the model to be fit by

INLA, i.e., the formula defines the terms in the linear predictor.

However, sometimes we need to modify the model so that linear combinations

of these terms are used instead of simply the ones set in the formula.

INLA allows this by defining a matrix A, which is called predictor matrix so that the actual linear

predictor \(\bm\eta^*\) used is

\[ \bm\eta^* = A \bm\eta \]

Here, \(\bm\eta\) is the linear predictor defined in the formula. By default, this matrix is the identity matrix.

Matrix A that defines the linear combinations to be used is passed using

element A in the list passed to argument control.predictor (see Section

2.5 for details). Matrix A can be a dense matrix or a sparse one

of the types implemented in the Matrix package (Bates and Maechler 2019). The dimension

of the A matrix must be \(n\times n\), with \(n\) the number of observations in

the model.

In order to provide a simple example we will consider the cement dataset

described in Section 2.3. A very simple use of the A matrix is

to re-scale the linear predictor used in the model (see Krainski et al. 2018 for

a similar example), for example, to have it multiplied by a constant. In this

case, we will take the A matrix as a diagonal matrix with values equal to 5.

This means that the linear predictors, as defined by the formula, will be

multiplied by 5, and that the estimates of the terms in the linear predictor

will shrink in a similar way so that the actual linear predictor \(A \bm\eta\)

remains the same as in the example in Section 2.3. Note that the

fitted values will also remain the same.

library("MASS")

library("Matrix")

data(cement)

A <- Diagonal(n = nrow(cement), x = 5)

summary(A)## 13 x 13 diagonal Matrix of class "ddiMatrix"

## Min. 1st Qu. Median Mean 3rd Qu. Max.

## 5 5 5 5 5 5Note how in the code above matrix A is a sparse matrix. Hence, the model

using this predictor matrix can be fit:

m1.A <- inla(y ~ x1 + x2 + x3 + x4, data = cement,

control.predictor = list(A = A))

summary(m1.A)##

## Call:

## "inla(formula = y ~ x1 + x2 + x3 + x4, data = cement,

## control.predictor = list(A = A))"

## Time used:

## Pre = 0.422, Running = 0.0601, Post = 0.0262, Total = 0.508

## Fixed effects:

## mean sd 0.025quant 0.5quant 0.975quant mode kld

## (Intercept) 12.482 13.997 -15.556 12.481 40.495 12.482 0

## x1 0.310 0.149 0.012 0.310 0.608 0.310 0

## x2 0.102 0.145 -0.188 0.102 0.391 0.102 0

## x3 0.020 0.151 -0.282 0.020 0.322 0.020 0

## x4 -0.029 0.142 -0.313 -0.029 0.255 -0.029 0

##

## Model hyperparameters:

## mean sd 0.025quant 0.5quant

## Precision for the Gaussian observations 0.209 0.093 0.068 0.195

## 0.975quant mode

## Precision for the Gaussian observations 0.428 0.167

##

## Expected number of effective parameters(stdev): 5.00(0.00)

## Number of equivalent replicates : 2.60

##

## Marginal log-Likelihood: -67.60Note how the estimates of the fixed effects are divided by 5 as compared

to the estimates obtained with the model fit in Section 2.3.

This is because of the effect of the A matrix.

In general, the predictor matrix can be useful for non-trivial examples. For example, the predictor matrix plays an important role in the development of spatial models based on stochastic partial differential equations (Krainski et al. 2018). See Chapter 7 for details.

6.3 Linear combinations

The use of the predictor matrix introduced in the previous section allows us to define models where the actual linear predictors are linear combinations of the effects in the model formula. However, in some situations we are only interested in computing linear combinations on some effects without altering model fitting.

With INLA, linear combinations on the different latent effects can be defined

and their posterior marginals estimated. Note that these linear combinations do

not alter the fit model (as the use of a predictor matrix did). Linear

combinations are passed using argument lincomb to the inla() function.

Furthermore, argument control.lincomb can be used to set the parameters that

control how posterior marginals of linear combinations are computed. Table

6.1 shows the options available to control

how the linear combinations are fit.

| Argument | Default | Description |

|---|---|---|

precision |

1e09 |

Tiny noise added to compute approximation |

verbose |

TRUE |

Use verbose if verbose is enabled globally. |

Linear combinations are defined by setting the effects and the associated

coefficients that they have to make the linear combination. Two functions are

available to define linear combinations: inla.make.lincomb(), to define a

single linear combination, and inla.make.lincombs(), to define several linear

combinations at once.

Function inla.make.lincomb() takes named arguments with the values of the

coefficients of the linear combination. The names are the names of the effects

to be used in the linear combination. For fixed effects, values must be a single number, while for random effects it is a vector of coefficients of the same

length as the index of the random effect. For those values of the random

effect not in the linear combination, NA must be used.

For example, in the analysis of the cement data above we might be interested

in computing the difference between coefficients of covariates x1 and

x2. This could be defined as follows:

inla.make.lincomb(x1 = 1, x2 = -1)If the linear combination involves a random effect index from 1 to \(p\),

the linear combination can be defined by including a term with the name

of the latent random effect. The value now is not a single number, but

a vector of length \(p\) with the coefficients of the different elements

of the random effects. Those elements that do not appear in the

linear combination must have a value of NA.

For example, if a random effect named u of length 4 is included in a

model and we want to compute the difference between its two terms, this

can be set up as:

inla.make.lincomb(u = c(1, -1, NA, NA))Function inla.make.lincombs() can be used to set more than one linear

combination at a time. Instead of using a single value for the linear

combinations on the fixed effects, a vector of coefficients can be passed.

For example, say that we are interested in comparing the coefficient of

variable x1 to the other three coefficients. In the design of experiments

literature these types of comparisons are often referred to as contrasts.

This can be set as several differences using linear combinations as follows:

inla.make.lincomb(

x1 = c( 1, 1, 1),

x2 = c(-1, 0, 0),

x3 = c( 0, -1, 0),

x4 = c( 0, 0, -1)

)Once the model has been fit, summaries of the linear combinations are available

in summary.lincomb.derived in the inla object returned. Similarly,

posterior marginals densities are available in marginals.lincomb.

Finally, two arguments can be passed through control.inla to control how

linear combinations are computed: lincomb.derived.only and

lincomb.derived.correlation.matrix. The first option indicates whether the

linear combinations are to be computed, and the second controls the computation

of the correlation matrix of the linear combinations. See Table

6.2 for a summary.

| Argument | Default | Description |

|---|---|---|

lincomb.derived.only |

TRUE |

Compute full graph of derived linear combinations. |

lincomb.derived.correlation.matrix |

FALSE |

Compute correlations for derived linear combinations. |

Linear combinations can be used for a number of issues, such as computing the posterior marginal of the linear predictor for a given set of covariate values. Another interesting application is to compare whether two effects are equal.

In order to provide a simple example, we will consider the abrasion dataset

(Davies 1954) from package faraway (Faraway 2016). This dataset records

data from an industrial experiment about wear of four different types of

materials after being fed into a wear testing machine. In each run,

four samples are processed, and the position of the samples may be important.

The different variables in this dataset are described in Table 6.3.

| Variable | Description |

|---|---|

run |

Run number (from 1 to 4). |

position |

Position number (from 1 to 4). |

material |

Type of material (A, B, C or D). |

wear |

Weight loss (in 0.1mm) over testing period. |

Given that the main interest is in the wear depending on the type of material,

material will be introduced into the model as a fixed effect, while run and

position are introduced as iid random affects. In addition, we have

noticed that default INLA priors produce too much shrinkage of the

coefficients and random effects towards zero, and the results do not reproduce

those in Faraway (2006). In particular, we have considered a larger precision on

the coefficients of the fixed effects. For the

prior on the precisions we have followed J. J. Faraway (2019b) and taken a Gamma prior

with parameters 0.5 and 95. This is an informative prior that has a mean

value half the variance of the residuals of a linear regression on wear

using material as predictor. The posterior means of precisions of the random

effects should be lower than this value. Furthermore, function

inla.hyperpar() has been used to obtain better estimates of the

hyperparameters once the model has been fit with INLA.

library("faraway")

data(abrasion)

# Prior prec. of random effects

prec.prior <- list(prec = list(param = c(0.5, 95)))

# Model formula

f.wear <- wear ~ -1 + material +

f(position, model = "iid", hyper = prec.prior) +

f(run, model = "iid", hyper = prec.prior)

# Model fitting

m0 <- inla(f.wear, data = abrasion,

control.fixed = list(prec = 0.001^2)

)

# Improve estimates of hyperparameters

m0 <- inla.hyperpar(m0)

summary(m0)##

## Call:

## "inla(formula = f.wear, data = abrasion, control.fixed = list(prec

## = 0.001^2))"

## Time used:

## Pre = 0.241, Running = 1.64, Post = 0.0965, Total = 1.98

## Fixed effects:

## mean sd 0.025quant 0.5quant 0.975quant mode kld

## materialA 265.7 9.784 246.0 265.7 285.3 265.7 0

## materialB 219.9 9.784 200.3 219.9 239.5 219.9 0

## materialC 241.7 9.784 222.0 241.7 261.3 241.7 0

## materialD 230.4 9.784 210.8 230.4 250.0 230.4 0

##

## Random effects:

## Name Model

## position IID model

## run IID model

##

## Model hyperparameters:

## mean sd 0.025quant 0.5quant

## Precision for the Gaussian observations 0.022 0.011 0.006 0.020

## Precision for position 0.008 0.006 0.001 0.006

## Precision for run 0.010 0.008 0.001 0.008

## 0.975quant mode

## Precision for the Gaussian observations 0.048 0.016

## Precision for position 0.025 0.004

## Precision for run 0.030 0.004

##

## Expected number of effective parameters(stdev): 9.28(0.43)

## Number of equivalent replicates : 1.72

##

## Marginal log-Likelihood: -98.70Then, we may be interested in comparing whether there is any difference between material A and any of the others. For example, the following linear constraint will compute the difference of the effects between material A and B:

lc <- inla.make.lincomb(materialA = 1, materialB = -1)This model can now be fit to compare materials A and B:

m0.lc <- inla.hyperpar(inla(f.wear, data = abrasion, lincomb = lc,

control.fixed = list(prec = 0.001^2)))

summary(m0.lc)##

## Call:

## "inla(formula = f.wear, data = abrasion, lincomb = lc,

## control.fixed = list(prec = 0.001^2))"

## Time used:

## Pre = 0.258, Running = 1.98, Post = 0.124, Total = 2.36

## Fixed effects:

## mean sd 0.025quant 0.5quant 0.975quant mode kld

## materialA 265.7 9.784 246.0 265.7 285.3 265.7 0

## materialB 219.9 9.784 200.3 219.9 239.5 219.9 0

## materialC 241.7 9.784 222.0 241.7 261.3 241.7 0

## materialD 230.4 9.784 210.8 230.4 250.0 230.4 0

##

## Linear combinations (derived):

## ID mean sd 0.025quant 0.5quant 0.975quant mode kld

## lc 1 45.75 5.455 34.78 45.75 56.73 45.75 0

##

## Random effects:

## Name Model

## position IID model

## run IID model

##

## Model hyperparameters:

## mean sd 0.025quant 0.5quant

## Precision for the Gaussian observations 0.022 0.011 0.006 0.020

## Precision for position 0.008 0.006 0.001 0.006

## Precision for run 0.010 0.008 0.001 0.008

## 0.975quant mode

## Precision for the Gaussian observations 0.048 0.016

## Precision for position 0.025 0.004

## Precision for run 0.030 0.004

##

## Expected number of effective parameters(stdev): 9.28(0.43)

## Number of equivalent replicates : 1.72

##

## Marginal log-Likelihood: -98.70Note that summary statistics of the posterior marginal of the linear combination can be accessed with

m0.lc$summary.lincomb.derived## ID mean sd 0.025quant 0.5quant 0.975quant mode kld

## lc 1 45.75 5.455 34.78 45.75 56.73 45.75 0This shows a positive posterior means and 95% credible interval that is above 0, which means that wear in material A is higher than in material B.

This can be extended to compare material A to all the other materials. This

can be represented by a \(3\times 4\) matrix to represent the 3 linear combinations required. Now inla.make.lincombs must be used in order to define

3 different linear combinations.

lcs <- inla.make.lincombs(

materialA = c( 1, 1, 1),

materialB = c(-1, 0, 0),

materialC = c( 0, -1, 0),

materialD = c( 0, 0, -1)

)The model is fit similarly to the previous example:

m0.lcs <- inla.hyperpar(inla(f.wear, data = abrasion, lincomb = lcs,

control.fixed = list(prec = 0.001^2)))

summary(m0.lcs)##

## Call:

## "inla(formula = f.wear, data = abrasion, lincomb = lcs,

## control.fixed = list(prec = 0.001^2))"

## Time used:

## Pre = 0.261, Running = 2.58, Post = 0.0931, Total = 2.94

## Fixed effects:

## mean sd 0.025quant 0.5quant 0.975quant mode kld

## materialA 265.7 9.784 246.0 265.7 285.3 265.7 0

## materialB 219.9 9.784 200.3 219.9 239.5 219.9 0

## materialC 241.7 9.784 222.0 241.7 261.3 241.7 0

## materialD 230.4 9.784 210.8 230.4 250.0 230.4 0

##

## Linear combinations (derived):

## ID mean sd 0.025quant 0.5quant 0.975quant mode kld

## lc1 1 45.75 5.455 34.78 45.75 56.73 45.75 0

## lc2 2 24.00 5.455 13.03 24.00 34.98 24.00 0

## lc3 3 35.25 5.455 24.28 35.25 46.23 35.25 0

##

## Random effects:

## Name Model

## position IID model

## run IID model

##

## Model hyperparameters:

## mean sd 0.025quant 0.5quant

## Precision for the Gaussian observations 0.022 0.011 0.006 0.020

## Precision for position 0.008 0.006 0.001 0.006

## Precision for run 0.010 0.008 0.001 0.008

## 0.975quant mode

## Precision for the Gaussian observations 0.048 0.016

## Precision for position 0.025 0.004

## Precision for run 0.030 0.004

##

## Expected number of effective parameters(stdev): 9.28(0.43)

## Number of equivalent replicates : 1.72

##

## Marginal log-Likelihood: -98.70Linear combinations can also be used to compare the levels of the random

effects. For example, let’s consider a comparison between positions 1 and

2. Variable position is an iid random effect with four different levels,

and the weights must be set in a vector of the same length. For those

levels that must be ignored in the linear combination, NA can be used.

Hence, to define a linear combination to compare levels 1 and 2 of variable

position we can define the linear combination as follows:

lc.pos <- inla.make.lincomb(position = c(1, -1, NA, NA))

m0.pos <- inla.hyperpar(inla(f.wear, data = abrasion, lincomb = lc.pos,

control.fixed = list(prec = 0.001^2)))

summary(m0.pos)##

## Call:

## "inla(formula = f.wear, data = abrasion, lincomb = lc.pos,

## control.fixed = list(prec = 0.001^2))"

## Time used:

## Pre = 0.247, Running = 1.88, Post = 0.0957, Total = 2.22

## Fixed effects:

## mean sd 0.025quant 0.5quant 0.975quant mode kld

## materialA 265.7 9.784 246.0 265.7 285.3 265.7 0

## materialB 219.9 9.784 200.3 219.9 239.5 219.9 0

## materialC 241.7 9.784 222.0 241.7 261.3 241.7 0

## materialD 230.4 9.784 210.8 230.4 250.0 230.4 0

##

## Linear combinations (derived):

## ID mean sd 0.025quant 0.5quant 0.975quant mode kld

## lc 1 -23.34 5.504 -33.67 -23.59 -11.62 -24.09 0

##

## Random effects:

## Name Model

## position IID model

## run IID model

##

## Model hyperparameters:

## mean sd 0.025quant 0.5quant

## Precision for the Gaussian observations 0.022 0.011 0.006 0.020

## Precision for position 0.008 0.006 0.001 0.006

## Precision for run 0.010 0.008 0.001 0.008

## 0.975quant mode

## Precision for the Gaussian observations 0.048 0.016

## Precision for position 0.025 0.004

## Precision for run 0.030 0.004

##

## Expected number of effective parameters(stdev): 9.28(0.43)

## Number of equivalent replicates : 1.72

##

## Marginal log-Likelihood: -98.70Fixed and random effects can be combined together to create more complex linear combinations. For example, the following linear combination considers the sum of the effect of material A, position 1 and run 2:

lc.eff <- inla.make.lincomb(materialA = 1, position = c(1, NA, NA, NA),

run = c(NA, 1, NA, NA))

m0.eff <- inla.hyperpar(inla(f.wear, data = abrasion, lincomb = lc.eff,

control.fixed = list(prec = 0.001^2)))

summary(m0.eff)##

## Call:

## "inla(formula = f.wear, data = abrasion, lincomb = lc.eff,

## control.fixed = list(prec = 0.001^2))"

## Time used:

## Pre = 0.248, Running = 1.82, Post = 0.101, Total = 2.17

## Fixed effects:

## mean sd 0.025quant 0.5quant 0.975quant mode kld

## materialA 265.7 9.784 246.0 265.7 285.3 265.7 0

## materialB 219.9 9.784 200.3 219.9 239.5 219.9 0

## materialC 241.7 9.784 222.0 241.7 261.3 241.7 0

## materialD 230.4 9.784 210.8 230.4 250.0 230.4 0

##

## Linear combinations (derived):

## ID mean sd 0.025quant 0.5quant 0.975quant mode kld

## lc 1 254 5.906 242.6 253.9 266.3 253.6 0

##

## Random effects:

## Name Model

## position IID model

## run IID model

##

## Model hyperparameters:

## mean sd 0.025quant 0.5quant

## Precision for the Gaussian observations 0.022 0.011 0.006 0.020

## Precision for position 0.008 0.006 0.001 0.006

## Precision for run 0.010 0.008 0.001 0.008

## 0.975quant mode

## Precision for the Gaussian observations 0.048 0.016

## Precision for position 0.025 0.004

## Precision for run 0.030 0.004

##

## Expected number of effective parameters(stdev): 9.28(0.43)

## Number of equivalent replicates : 1.72

##

## Marginal log-Likelihood: -98.706.4 Several likelihoods

So far, we have considered models with a single likelihood but INLA can

handle models with more than one likelihood. This is useful to define

joint models (see Chapter 10) in which one likelihood

models survival time and the second one models longitudinal data.

The first likelihood will be that of a survival model, while the second

one will be of the types used to model longitudinal data.

When using several likelihoods data must be stored in a very particular way.

First of all, the response variable must be a matrix with as many columns as

likelihoods. Hence, the first column will be the response used by the first

likelihood and so on. Data must be stored so that there is one variable per

column and a single value of any of the variables per row. All the empty

elements in the matrix are set to NA.

For example, let us consider a joint model with response variables \(\mathbf{y} = (y_1\ldots, y_n)\) and \(\mathbf{z} = (z_1,\ldots, z_m)\). Then, data must be stored in a matrix like the following:

\[ \left[ \begin{array}{cc} y_1 & \mathtt{NA}\\ \vdots & \mathtt{NA}\\ y_n & \mathtt{NA}\\ \mathtt{NA} & z_1\\ \mathtt{NA} & \vdots\\ \mathtt{NA} & z_m\\ \end{array} \right] \]

Note that the dimension of this matrix is \((n + m) \times 2\), i.e., the number of rows is the total number of observations and the number of columns is equal to the number of variables. This can be easily generalized to any number of response variables.

When multiple likelihoods are used in a model, these are passed in a vector

to argument family. For example, the following code could be used to fit

a model with a Gaussian and a Poisson likelihood:

family = c("gaussian", "poisson")As stated above, the response variables need to be formatted in a particular way. A matrix with as many likelihoods as columns is required. The number of rows is the total number of observations for all likelihoods. If in the example above there are 30 observations from a Gaussian likelihood and 20 from a Poisson one, then the response must be a matrix with 2 columns and 50 rows.

Then, observations are stacked in a matrix so that the observations from the

Gaussian likelihood are in the first column and rows 1 to 30. Then, observations

for the Poisson likelihood are in the second column and rows 31 to 50. All the

other elements in the matrix are filled with NA. This ensures that every

row has only a single observed value. Note that then there is an implicit

index from 1 to 50 to identify each one of the observations, regardless of

the likelihood they belong to.

In order to define the model, all terms for both likelihoods need to be

included in the linear predictor. Hence, when defining indices for the latent

random effects, this can go (for example) from 1 to the total number of rows in

the response matrix. When a covariate only affects

observations in a single likelihood, the values for the observations in the

other likelihoods must be set to NA. Similarly, the indices of the latent

random effects must be set to NA for those observations that do not depend

on the latent random effect.

6.4.1 Simulated example

To illustrate the use of several likelihoods we will develop an example here using two (independent) variables from a Gaussian and Poisson likelihood, respectively. First of all, 30 observations from a standard Gaussian distribution and 20 observations from a Poisson with mean 10 will be drawn:

set.seed(314)

# Gaussian data

d1 <- rnorm(30)

# Poisson data

d2 <- rpois(20, 10)Next, the two response variables will be put in a 2-column matrix as

required by INLA:

# Data

d <- matrix(NA, ncol = 2, nrow = 30 + 20)

d[1:30, 1] <- d1

d[30 + 1:20, 2] <- d2In order to have two different intercepts in the model it is necessary to add

them as two separate covariates. In this case, both intercepts have all

values equal to one, but the same principle would apply when two separate

coefficients are required for the same covariate or when random effects only

apply to data in one the likelihoods. Values NA mean that the covariate does

not appear in the linear predictor of the response.

# Define a different intercept for each likelihood

Intercept1 <- c(rep(1, 30), rep(NA, 20))

Intercept2 <- c(rep(NA, 30), rep(1, 20))If the coefficient is to be the same, shared between both likelihoods, then the

covariate is replicated as many times as likelihoods in the model, so that it

is a vector. For example, the next variable x will be shared by both terms

because it is a vector of simulated data of length 50 (the total number of

observations):

x <- rnorm(30 + 20)Finally, the model is defined and fit below. Note how the data is now

passed using a list as a data.frame would not be suitable in this case

because the response is a matrix.

mult.lik <- inla(Y ~ -1 + I1 + I2 + x,

data = list(Y = d, I1 = Intercept1, I2 = Intercept2, x = x),

family = c("gaussian", "poisson"))

summary(mult.lik)##

## Call:

## c("inla(formula = Y ~ -1 + I1 + I2 + x, family = c(\"gaussian\",

## \"poisson\"), ", " data = list(Y = d, I1 = Intercept1, I2 =

## Intercept2, x = x))" )

## Time used:

## Pre = 0.197, Running = 0.0827, Post = 0.0171, Total = 0.297

## Fixed effects:

## mean sd 0.025quant 0.5quant 0.975quant mode kld

## I1 -0.316 0.161 -0.635 -0.316 0.003 -0.316 0

## I2 2.222 0.077 2.067 2.223 2.369 2.225 0

## x 0.021 0.071 -0.118 0.021 0.159 0.021 0

##

## Model hyperparameters:

## mean sd 0.025quant 0.5quant

## Precision for the Gaussian observations 1.36 0.346 0.769 1.33

## 0.975quant mode

## Precision for the Gaussian observations 2.12 1.27

##

## Expected number of effective parameters(stdev): 3.00(0.00)

## Number of equivalent replicates : 16.66

##

## Marginal log-Likelihood: -117.94Note that the second intercept (for the Poisson likelihood) is close to the

logarithm of the actual mean and not the actual mean of the Poisson likelihood.

Also, there is a single coefficient for x because it is shared by both parts

of the model. The point estimate is very close to zero because the covariate

had no effect on the response when the data were simulated.

6.5 Shared terms

When a model with several likelihoods is defined, it may be necessary to share

some terms among the different parts of the model. This can be implemented

using the copy and replicate features. In both cases the linear predictors

of the different likelihoods will share the same type of latent effect. The

main differences between the copy and replicate features is that with the

copy effect the values of the random effects are the same but copied effects

can be scaled by a parameter. This also means that all copies of the random

effects will share the same hyperparameters. The replicate effect will have

different hyperparameters for each replicate of the effect. These two features

are described in more detail below.

6.5.1 Copy feature

The copy feature allows for the inclusion of a shared term among

several linear predictors. In practice, this is implemented by

defining the effect as part of a linear predictor and then making a

copy of it in another linear predictor. The copy is the copied effect

plus some tiny noise. Optionally, the copied effect can be multiplied by

a scale parameter that can be set to a fixed value or estimated

from the data.

More formally, let’s assume that we have a latent effect \(\mathbf{u} = (u_1,\ldots, u_p)\), where \(p\) is the length of the latent effect. Then, the copied effect \(\mathbf{u}^*\) is defined to be

\[ u_j^* = \beta u_{j(i)} + \varepsilon_j,\ j=1,\ldots,n \]

Here, \(n\) is the number of data observations, and \(j(i)\) is the index (between

1 and \(p\)) of the copied latent effect. Note that the copied effect does not

necessarily have the same indexing as the original effect and that, in fact,

only parts of it can be copied. \(\varepsilon_j\) is a tiny error that is added

with a large precision for computational reasons. This precision is set in

option precision in the call to the f() function when the copied effect is

defined, with a default value of \(\exp(14)\) (see Chapter 3).

Note that several copies of the same effect can be made and that all these effects (e.g., original and copies) will share the same hyperparameters. This means that the effect will be estimated from all the data observations that share this effect.

The copy effect is defined as:

f(idx2, copy = "idx")Here, "idx" is the name of the index variable used in the original effect

(as a character variable) and

idx2 is another index that must take values in the same set as idx.

However, the values in idx2 do not necessarily have the same ordering

and that only the elements of \(\mathbf{u}\) indexed in idx2 will be copied.

Coefficient \(\beta\) of the copied effects can be estimated or set to a fixed

number by using argument hyper to define its prior distribution (see Chapter

5 for details). By setting fixed to TRUE in the definition of

the prior, \(\beta\) will be set to the value specified in initial. Table

6.4 shows the default values of the prior on \(\beta\), which is

setting the hyperparameter to a fixed value of 1. Thus, the part of the

definition that sets a Gaussian prior distribution with parameters 1 and 10 is

ignored (unless fixed is set to FALSE).

| Argument | Default value |

|---|---|

initial |

1 |

fixed |

TRUE |

prior |

"normal" |

params |

c(1, 10) |

As a simple example on the use of the copy feature we will use a simulated

dataset that shares a common coefficient. The data set is made of Gaussian and

Poisson observations that depend on a common covariate. In particular,

this is the model:

\[\begin{eqnarray*} y_i \sim N(\mu_i, \tau = 1) & i = 1,\ldots, 150\\ \mu_i = 2\cdot x_i & i = 1,\ldots, 150\\ y_i \sim Po(\lambda_i) & i = 151,\ldots, 200\\ \log(\lambda) = 2\cdot x_i & i = 151,\ldots, 200\\ \end{eqnarray*}\]

Note that in this case, the copied effect is the coefficient of covariate

\(x_i\) in the linear predictors. This coefficient is the same in the two

parts of the model and parameter \(\beta\) of the copy effect should be

close to 1.

First of all, data are simulated from the model above:

set.seed(271)

#Covariate

xx <- runif(200, 1, 2)

#Gaussian data

y.gaus <- rnorm(150, mean = 2 * xx[1:150])

#Poisson data

y.pois <- rpois(50, lambda = exp(2 * xx[151:200]))Note that in the previous code the mean of the Poisson takes into account that the effect of the covariate included in the linear predictor is linked to the mean using a non-linear function.

Next, the response variable must be stored in a two-column matrix as this is a model with two likelihoods (see Section 6.4).

y <- matrix(NA, ncol = 2, nrow = 200)

y[1:150, 1] <- y.gaus

y[151:200, 2] <- y.poisNote that in order to be able to use the copy feature, the latent effect must

be defined through the f() function. Hence, the latent effect will be an

iid with an index vector with all values equal to 1, which will be the

coefficient of the covariate. For this reason, the values of the covariates are

introduced as weights in the latent effect inside the f() function. This

requires the creation of two indices for the Gaussian and Poisson observations:

idx.gaus <- c(rep(1, 150), rep(NA, 50))

idx.pois <- c(rep(NA, 150), rep(1, 50))Note that index idx.gaus is 1 for all Gaussian observations and NA for the

Poisson ones. This makes that the latent effect defined with this one only

affect the Gaussian observations. Index idx.pois works in a similar way but

only affects the Poisson observations.

Given that both indices only have a single value, the latent effect will only

be \(u_1\), that appears in the linear predictor multiplying covariate \(x_i\),

i.e., the linear predictor in the Gaussian likelihood will be \(u_1\cdot x_i\).

The copied part of the model will then be \(\beta \cdot(u_1\cdot x_i)\), in the

linear predictor of the Poisson likelihood. Note that in the example we also

want to estimate \(\beta\); we need to set fixed to FALSE in its prior

definition so that it is actually estimated.

Finally, the model is fit with INLA. The call to inla() and summary of the

resulting model are:

m.copy <- inla(y ~ -1 + f(idx.gaus, xx, model = "iid") +

f(idx.pois, xx, copy = "idx.gaus",

hyper = list(beta = list(fixed = FALSE))),

data = list(y = y, xx = xx),

family = c("gaussian", "poisson")

)

summary(m.copy)##

## Call:

## c("inla(formula = y ~ -1 + f(idx.gaus, xx, model = \"iid\") +

## f(idx.pois, ", " xx, copy = \"idx.gaus\", hyper = list(beta =

## list(fixed = FALSE))), ", " family = c(\"gaussian\", \"poisson\"),

## data = list(y = y, xx = xx))" )

## Time used:

## Pre = 0.28, Running = 0.253, Post = 0.0213, Total = 0.554

## Random effects:

## Name Model

## idx.gaus IID model

## idx.pois Copy

##

## Model hyperparameters:

## mean sd 0.025quant 0.5quant

## Precision for the Gaussian observations 0.988 0.114 0.774 0.985

## Precision for idx.gaus Inf NaN 0.000 0.000

## Beta for idx.pois 1.024 0.029 0.968 1.023

## 0.975quant mode

## Precision for the Gaussian observations 1.22 0.984

## Precision for idx.gaus Inf NaN

## Beta for idx.pois 1.08 1.022

##

## Expected number of effective parameters(stdev): 1.01(0.00)

## Number of equivalent replicates : 198.11

##

## Marginal log-Likelihood: -372.87The estimates of the coefficients of the model are not shown in the model

summary because they are included now as a random effect. Note that

parameter \(\beta\) of the copy feature has a posterior mean very close to 1.

The estimates of the coefficient (original and copy) are shown as:

m.copy$summary.random## $idx.gaus

## ID mean sd 0.025quant 0.5quant 0.975quant mode kld

## 1 1 1.989 0.04746 1.898 1.989 2.079 1.988 7.528e-08

##

## $idx.pois

## ID mean sd 0.025quant 0.5quant 0.975quant mode kld

## 1 1 2.032 0.0159 2.001 2.032 2.063 2.032 6.333e-07Two important things should be noted now. First of all, the estimates are

almost identical, with the only difference that the effect idx.pois is

a copy of idx.gaus which includes some tiny added noise. Secondly, both

point estimates are very close to the actual value of the coefficient,

which is 2. Hence, the model works as expected.

6.5.2 Replicate feature

The replicate effect is similar to the copy effect but now the replicated

effects only share the hyperparameters. This means that the values of the

random effects in the different replicates can be different. Replicates of the

same latent effect are defined with argument replicate in the definition of

the latent effect, which takes a vector of integer values with the different

groups that define the replicas. Hence, the hyperparameters will be informed

by all the observations but the actual estimates of the latent effects can vary

between groups.

Given a set of \(K\) replicated random effects \(\mathbf{u}_1,\ldots,\mathbf{u}_K\) and hyperparameters \(\theta_r\), the distribution of the random effects can be written down as

\[ \mathbf{u}_k \sim f(\theta_r),\ k=1,\ldots,K \]

Note that each of the \(\mathbf{u}_k\) is a vector of values and that the hyperparameters \(\theta_r\) may be a vector as well. Also, \(f(\theta_r)\) represents the distribution of the random effects given the hyperparameters \(\theta_r\), that are shared by all replicated effects. Note that the length of the different \(\mathbf{u}_k\) is the same as the length of the longest replicated random effect. For example, if two random effects are replicated and \(\mathbf{u}_1\) is indexed from 1 to \(30\) and \(\mathbf{u}_2\) only from 1 to 20, then \(\mathbf{u}_2\) will have 10 extra elements that will not be estimated from the data (and treated as modeling missing observations).

The replicate index must take consecutive integer values starting from 1 to \(K\), the number of replicas, and the number of replicated effects created is the maximum value in the index of the replicate effect.

The NelPlo dataset (Koop and Steel 1994) in the dlm package (Petris, Petrone, and Campagnoli 2009; Petris 2010) contains a subset of the dataset with the same name in the tseries

package that will be used to show the use of the replicate feature.

The two variables included in the time series measure industrial production

(ip), using a transformation of the original time series, and stock prices (stock.prices), as measured by the S&P500 index. The variables in the dataset

are summarized in Table 6.5.

| Variable | Description |

|---|---|

ip |

Industrial production from 1946 to 1988. Transformed from the original series by taking 100 * diff(log()). |

stock.prices |

Stock prices (S&P500 index) from 1946 and 1988. |

The dataset can be loaded and summarized with the following code:

library("dlm")

data(NelPlo, package = "dlm")

summary(NelPlo)## ip stock.prices

## Min. :-4.390 Min. :-5.71

## 1st Qu.: 0.261 1st Qu.:-0.58

## Median : 1.065 Median : 1.56

## Mean : 0.791 Mean : 1.67

## 3rd Qu.: 1.854 3rd Qu.: 3.71

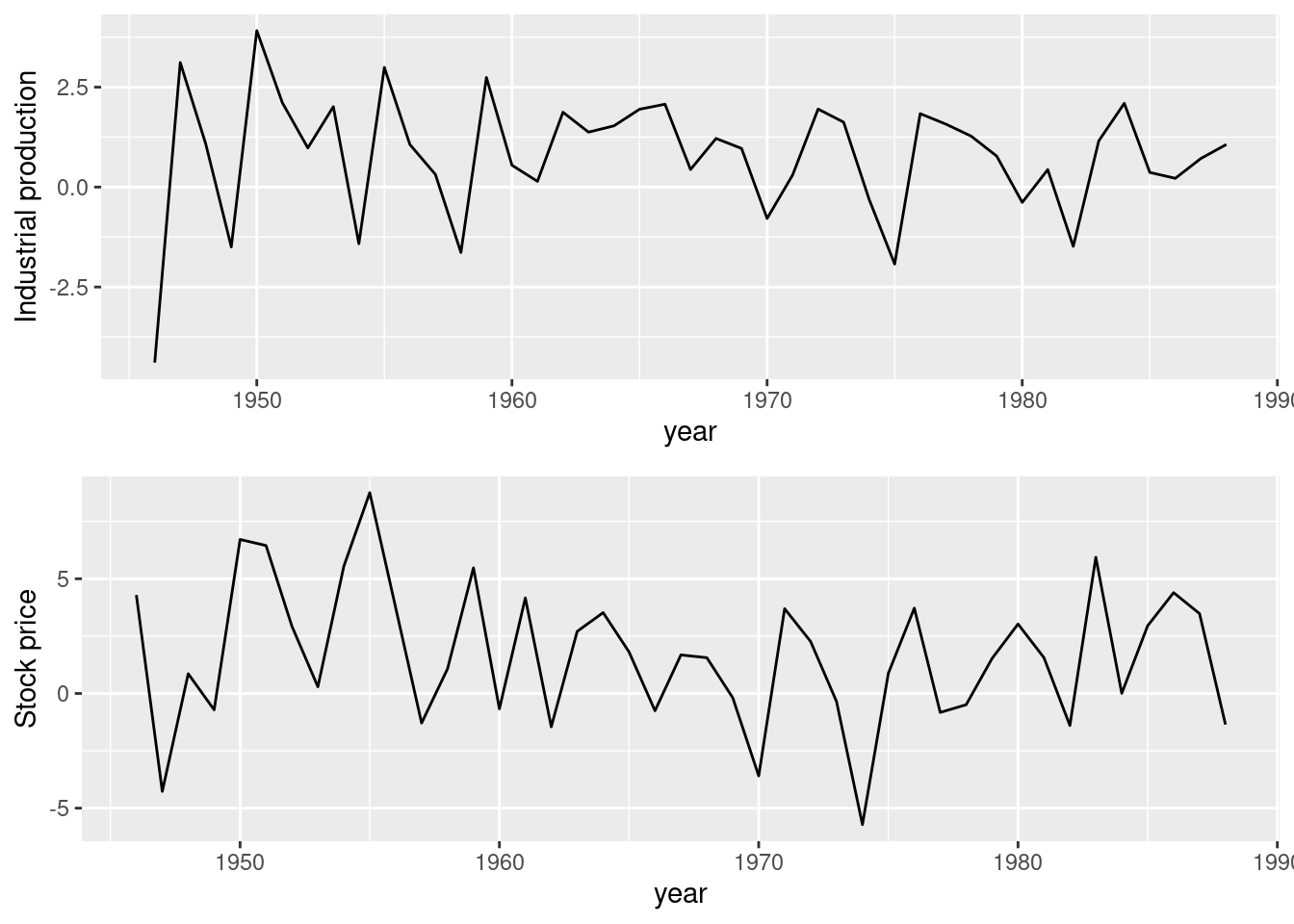

## Max. : 3.914 Max. : 8.76Figure 6.1 shows the two times series in the dataset, which seem

to have a similar behavior. For this reason, a model with different intercepts

but replicated ar1 latent effect will be fit. Hence, this model assumes that

the temporal correlation of the data is similar.

Figure 6.1: Time series of industrial production and stock prices in the NelPlo dataset.

The model will be fit using a single Gaussian likelihood so the data needs to be put as a single vector as well.

nelplo <- as.vector(NelPlo)Next, the indices for the ar1 latent effect and the replicate effects are

defined. This is done by taking the number of year first, n, and then creating

the required indices. The index for the ar1 latent effect will go from 1

to \(n\) (and will be repeated once to cover both time series). The

index for the replicate effect will go from 1 to 2, with the first \(n\)

values having an index of 1 and the last \(n\) values of the data having

an index of 2.

#Number of years

n <- nrow(NelPlo)

#Index for the ar1 latent effect

idx.ts <- rep(1:n, 2)

# Index for the replicate effect

idx.rep <- rep(1:2, each = n)Two new variables are created to include two different intercepts for each part of the data:

# Intercepts

i1 <- c(rep(1, n), rep(NA, n))

i2 <- c(rep(NA, n), rep(1, n))Finally, the model is fit as seen below. The fitted values are also computed

(using the options in control.compute) and a vague prior on

the precision of the random effects has been used (as described in

Chapter 3).

m.rep <- inla(nelplo ~ -1 + i1 + i2 +

f(idx.ts, model = "ar1", replicate = idx.rep,

hyper = list(prec = list(param = c(0.001, 0.001)))),

data = list(nelplo = nelplo, i1 = i1, i2 = i2, idx.ts = idx.ts,

idx.rep = idx.rep),

control.predictor = list(compute = TRUE)

)

summary(m.rep)##

## Call:

## c("inla(formula = nelplo ~ -1 + i1 + i2 + f(idx.ts, model =

## \"ar1\", ", " replicate = idx.rep, hyper = list(prec = list(param

## = c(0.001, ", " 0.001)))), data = list(nelplo = nelplo, i1 = i1,

## i2 = i2, ", " idx.ts = idx.ts, idx.rep = idx.rep),

## control.predictor = list(compute = TRUE))" )

## Time used:

## Pre = 0.229, Running = 0.248, Post = 0.0295, Total = 0.506

## Fixed effects:

## mean sd 0.025quant 0.5quant 0.975quant mode kld

## i1 0.790 0.369 0.064 0.790 1.516 0.790 0

## i2 1.674 0.369 0.948 1.674 2.399 1.674 0

##

## Random effects:

## Name Model

## idx.ts AR1 model

##

## Model hyperparameters:

## mean sd 0.025quant

## Precision for the Gaussian observations 0.178 2.60e-02 0.131

## Precision for idx.ts 68.816 3.41e+10 8.352

## Rho for idx.ts 0.033 6.78e-01 -0.986

## 0.5quant 0.975quant mode

## Precision for the Gaussian observations 0.176 0.233 0.174

## Precision for idx.ts 56.624 195.185 28.259

## Rho for idx.ts 0.087 0.976 -0.998

##

## Expected number of effective parameters(stdev): 2.41(0.452)

## Number of equivalent replicates : 35.64

##

## Marginal log-Likelihood: -223.14

## Posterior marginals for the linear predictor and

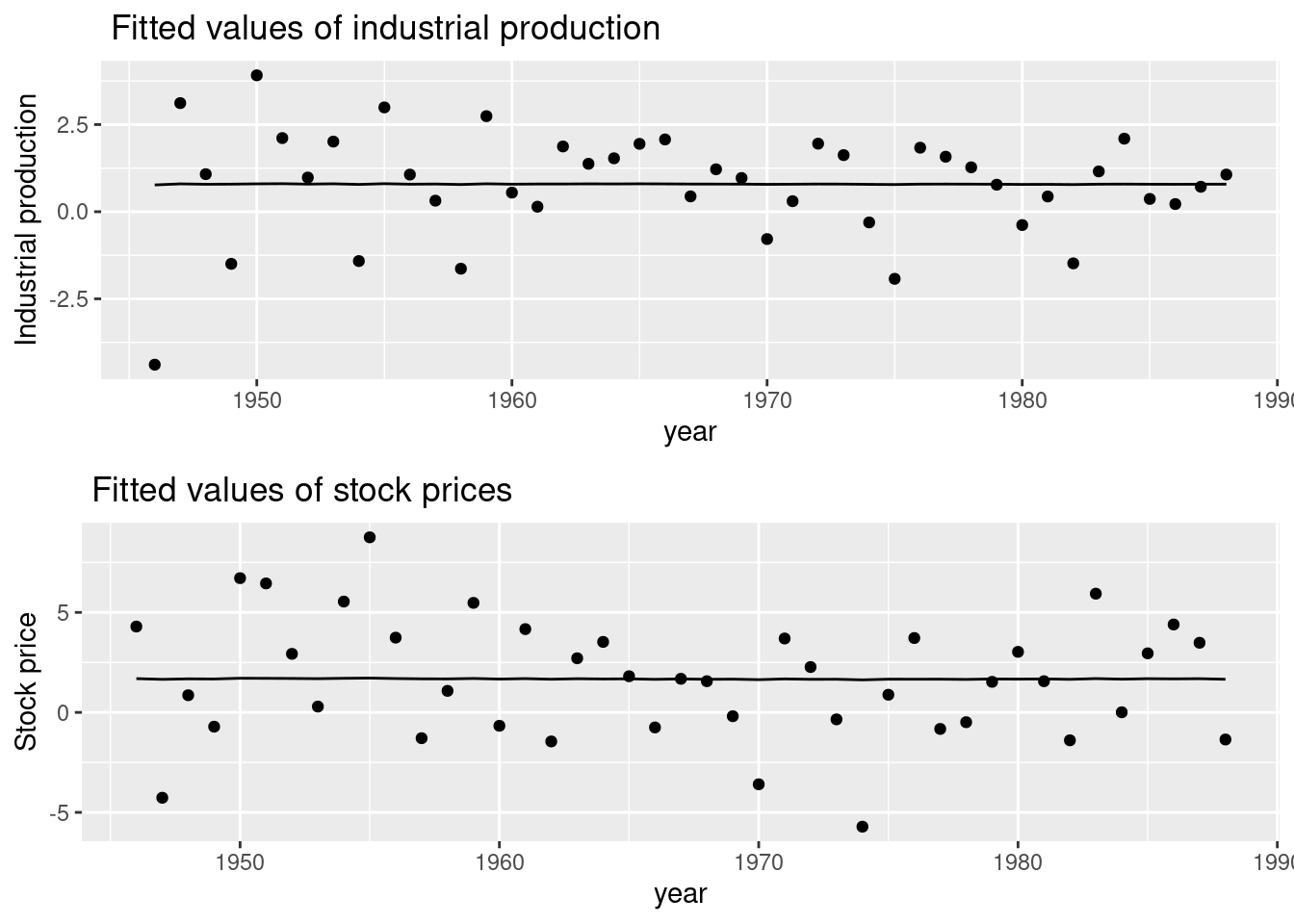

## the fitted values are computedThe model fit shows different estimates of the intercepts, which we had

anticipated. However, the hyperparameters of the ar1 are shared between both

time series.

Figure 6.2 shows the fitted values together with the observed values. It seems that the fitted values overfit the observed data, but see Chapter 8 and Chapter 9 for a discussion of these models and how to avoid overfitting. In general, overfitting can be avoided by setting specific priors on the model hyperparameters.

Figure 6.2: Fitted values (i.e., posterior means) to the variables in the NelPlo dataset using the replicate feature in INLA.

6.6 Linear constraints

As introduced in Chapter 3, additional linear constraints on the latent effects can be imposed. Given a latent effect \(\mathbf{u}\), the linear constraint is defined as

\[ \mathbf{A} \mathbf{u}^{\top} = \mathbf{e}^{\top} \]

where \(\mathbf{A}\) is a matrix with the same number of columns as the length of the latent effect \(\mathbf{u}\). Hence, the number of rows represents the number of linear constraints on the latent effect and \(\mathbf{e}\) is a vector of values that is defined accordingly.

Both \(\mathbf{A}\) and \(\mathbf{e}\) are passed through argument extraconstr

using a named list with values A and e in the the definition of the

latent effect using function f(). Note that there is another

argument constr which can be used to add a sum-to-zero constraint on

the latent effect by setting it to TRUE. This argument is set to

TRUE for some latent effects (such as, for example, the rw1

and besag latent effects and other intrinsic effects). In case of doubt,

the default option can be seen in the documentation available via the

inla.doc() function.

| Argument | Default | Description |

|---|---|---|

constr |

Depends on latent effect. | Add sum-to-zero constraint. |

extraconstr |

list(A = NULL, e = NULL) |

Add extra constraints on the random effect. |

Adding linear constraints is important in some cases as this makes the different effects in a model identifiable. Rue and Held (2005) describe this topic in detail. Furthermore, see Knorr-Held (2000) and Ugarte et al. (2014) on the role of imposing linear constraints to spatio-temporal latent effects, but these principles could also be applied to other types of latent effects. Also, Goicoa et al. (2018) note that adding additional constraints on the latent effects may produce different estimates than expected and caution should be taken when setting additional linear constraints.

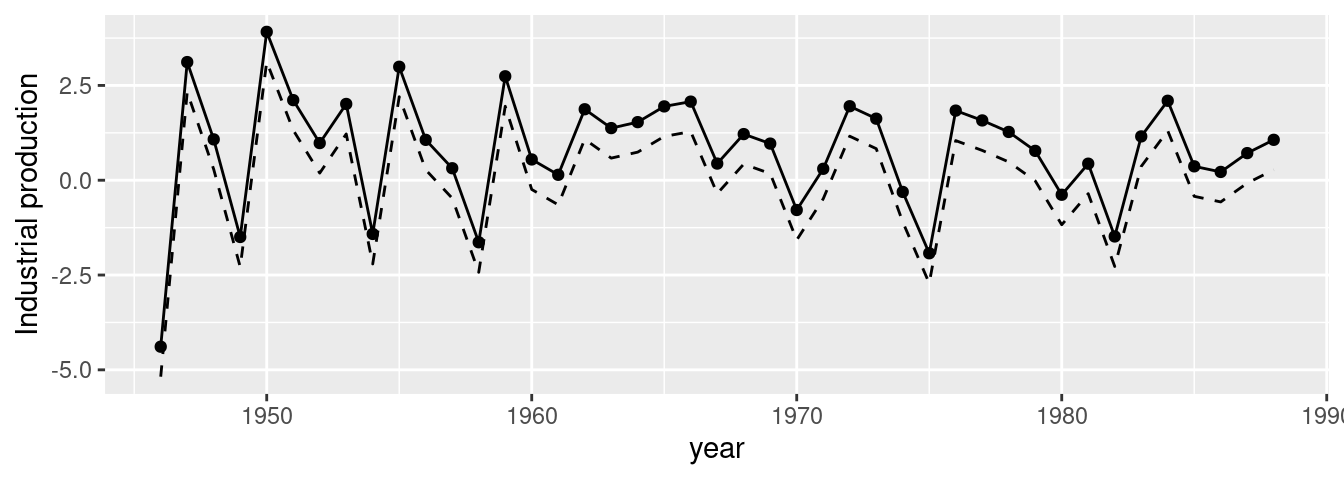

As a simple example, we will add a sum to zero constraint to the ar1

model fit to the NelPLo dataset. In this case only the industrial production

will be considered. We will also remove the intercept to show the effect of

constraining the random effect.

First, the matrix A and vector e need to be defined:

# Define values of A and e to set linear constraints

A <- matrix(1, ncol = n, nrow = 1)

e <- matrix(0, ncol = 1)Next, the model is fit using argument extraconstr in the call to the

f() function that defines the latent effect. Remember that the intercept

has the sole purpose of making the effect of the sum-to-zero constraint

more evident.

m.unconstr <- inla(ip ~ -1 + f(idx, model = "ar1"),

data = list(ip = NelPlo[, 1], idx = 1:n),

control.family = list(hyper = list(prec = list(initial = 10,

fixed = TRUE))),

control.predictor = list(compute = TRUE)

)

m.constr <- inla(ip ~ -1 + f(idx, model = "ar1",

extraconstr = list(A = A, e = e)),

data = list(ip = NelPlo[, 1], idx = 1:n),

control.family = list(hyper = list(prec = list(initial = 10,

fixed = TRUE))),

control.predictor = list(compute = TRUE)

)Figure 6.3 shows the estimates of the random effects from both models. Note how now imposing the sum-to-zero constraint seems to provide slightly different estimates from the unconstrained estimates. It is possible that the estimates of other parameters in the model also change as a result of imposing a constraint on the random effects, as described in Goicoa et al. (2018).

Figure 6.3: Comparison between two random effects estimates using a sum-to-zero constraint (solid line) and no constraint (dashed lines).

6.7 Final remarks

The features presented in this chapter can help to build more complex models

using INLA. These are extensively used in some of the models used in other

parts of the book. When the latent effect has a very complex structure

that does not fit any of the latent effects described so far with the

help of these additional features, there are a number of ways to implement

custom latent effects for INLA. These methods are described in

Chapter 11.

References

Bates, Douglas, and Martin Maechler. 2019. Matrix: Sparse and Dense Matrix Classes and Methods. https://CRAN.R-project.org/package=Matrix.

Davies, O. L. 1954. The Design and Analysis of Industrial Experiments. Wiley.

Faraway, J. 2006. Extending the Linear Model with R. Chapman; Hall, London.

Faraway, Julian. 2016. Faraway: Functions and Datasets for Books by Julian Faraway. https://CRAN.R-project.org/package=faraway.

Faraway, Julian J. 2019b. “INLA for Linear Mixed Models.” http://www.maths.bath.ac.uk/~jjf23/inla/.

Goicoa, T., A. Adin, M. D. Ugarte, and J. S. Hodges. 2018. “In Spatio-Temporal Disease Mapping Models, Identifiability Constraints Affect PQL and INLA Results.” Stochastic Environmental Research and Risk Assessment 3 (32): 749–70.

Knorr-Held, Leonhard. 2000. “Bayesian Modelling of Inseparable Space-Time Variation in Disease Risk.” Statistics in Medicine 19 (17‐18): 2555–67.

Koop, G., and M. F. J. Steel. 1994. “A Decision-Theoretic Analysis of the Unit-Root Hypothesis Using Mixtures of Elliptical Models.” Journal of Business and Economic Statistics 12: 95–107.

Krainski, Elias T., Virgilio Gómez-Rubio, Haakon Bakka, Amanda Lenzi, Daniela Castro-Camilo, Daniel Simpson, Finn Lindgren, and Håvard Rue. 2018. Advanced Spatial Modeling with Stochastic Partial Differential Equations Using R and INLA. Boca Raton, FL: Chapman & Hall/CRC.

Petris, Giovanni. 2010. “An R Package for Dynamic Linear Models.” Journal of Statistical Software 36 (12): 1–16. http://www.jstatsoft.org/v36/i12/.

Petris, Giovanni, Sonia Petrone, and Patrizia Campagnoli. 2009. Dynamic Linear Models with R. UseR! Springer-Verlag, New York.

Rue, H., and L. Held. 2005. Gaussian Markov Random Fields: Theory and Applications. Chapman; Hall/CRC Press.

Ugarte, M. D., A. Adin, T. Goicoa, and A. F. Militino. 2014. “On Fitting Spatio-Temporal Disease Mapping Models Using Approximate Bayesian Inference.” Statistical Methods in Medical Research 23: 507–30. https://doi.org/10.1177/0962280214527528.